Game Developer is part of the Informa Tech Division of Informa PLC

Informa PLC

|

ABOUT US

|

INVESTOR RELATIONS

|

TALENT

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Game Market Research

GDC Vault

GDC

Advertise With Game Developer

Stay Updated

Stay Updated

News

Trending

Related Topics

Game Industry Layoffs

GDC 2024 Coverage

Generative AI

Investments & Aquisitions

Unionization

Top Stories

Business

Game Design

Marketing

Programming

More

Related Topics

Interviews

Q&A's

Deep Dives

Postmortems

Culture

Business

Marketing

Design

Programming

Production

Art

Audio

Recent in

More

Read More: Business

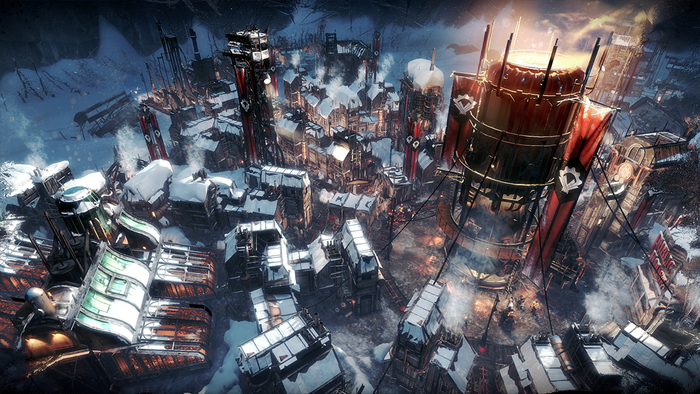

A city fighting back the cold in Frostpunk

Business

Frostpunk has topped 5 million sales in six years

Frostpunk has topped 5 million sales in six years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Key artwork for Garry's Mod

Business

Nintendo's legal team is coming for Garry's Mod after 20 years

Nintendo's legal team is coming for Garry's Mod after 20 years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Blogs

Related Topics

All Blogs

Featured Blogs

Blogging Guidelines

Blog Now

See All

Jobs

Related Topics

Game Artist

Game Animation

Video Game Designer

Game Programmer

Gameplay Engineer

Education

More Jobs

See All

Sponsored By

Home

Game Platforms

Game Platforms

More Topics

Console

PC

Mobile

Extended Reality

Cloud

A city fighting back the cold in Frostpunk

Business

Frostpunk has topped 5 million sales in six years

Frostpunk has topped 5 million sales in six years

Dictatorship and chill?

by

Chris Kerr

Apr 25, 2024

|

2 Min Read

Key artwork for Garry's Mod

Business

Nintendo's legal team is coming for Garry's Mod after 20 years

Nintendo's legal team is coming for Garry's Mod after 20 years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Headshot of Ubisoft veteran (and executive VP) Cécile Russeil.

Business

Ubisoft appoints Cécile Russeil as new executive VP

Ubisoft appoints Cécile Russeil as new executive VP

by

Justin Carter

Apr 24, 2024

1 Min Read

Logo for the Embracer Group.

Business

Lars Wingefors says splitting Embracer was for the greater good...of business

Lars Wingefors says splitting Embracer was for the greater good...of business

by

Justin Carter

Apr 24, 2024

2 Min Read

Graphic of games made and released under browser developer Arkadium Games.

Business

Arkadium launches platform for third-party browser game devs

Arkadium launches platform for third-party browser game devs

by

Justin Carter

Apr 24, 2024

1 Min Read

A Brotherhood of Steel Knight in Fallout 76.

Business

Fallout 76 hits 1 million players in a day, brings overall series to near-5 million players

Fallout 76 hits 1 million players in a day, brings overall series to near-5 million players

by

Justin Carter

Apr 24, 2024

1 Min Read

Business

Valve updates Steam refund policy to cover 'Advanced Access' playtime

Valve updates Steam refund policy to cover 'Advanced Access' playtime

Apr 24, 2024

|

2 Min Read

by

Chris Kerr

Business

Microsoft is cutting jobs at Bethesda France

Microsoft is cutting jobs at Bethesda France

Apr 24, 2024

|

2 Min Read

by

Chris Kerr

Business

Kazuma Kaneko, longtime Atlus artist, departs after 35-year run

Kazuma Kaneko, longtime Atlus artist, departs after 35-year run

Apr 23, 2024

|

2 Min Read

by

Justin Carter

Business

Apple reaffirms faith in Arcade, says Vision Pro included in platform plans

Apple reaffirms faith in Arcade, says Vision Pro included in platform plans

Apr 23, 2024

|

2 Min Read

by

Justin Carter

Business

Flaming Fowl lays off staff after unveiling demo for its (shelved) game

Flaming Fowl lays off staff after unveiling demo for its (shelved) game

Apr 23, 2024

|

2 Min Read

by

Justin Carter

Business

Alone in the Dark dev Pieces lays off staff following revival's release

Alone in the Dark dev Pieces lays off staff following revival's release

Apr 23, 2024

|

1 Min Read

by

Justin Carter

Extended Reality

Meta expanding mixed reality ecosystem under Meta Horizon OS banner

Meta expanding mixed reality ecosystem under Meta Horizon OS banner

Apr 23, 2024

|

3 Min Read

by

Chris Kerr

Business

ESA says members won’t support any plan for libraries to preserve games online

ESA says members won’t support any plan for libraries to preserve games online

Apr 22, 2024

|

4 Min Read

by

Justin Carter

Business

Strange Scaffold's El Paso, Elsewhere is becoming a movie

Strange Scaffold's El Paso, Elsewhere is becoming a movie

Apr 22, 2024

|

1 Min Read

by

Justin Carter

Business

Atomicom changes name to Starlight Games, gains Wipeout co-creator Nick Burcombe

Atomicom changes name to Starlight Games, gains Wipeout co-creator Nick Burcombe

Apr 22, 2024

|

2 Min Read

by

Justin Carter

Business

Krafton acquires minority stake in Forever Skies developer Far From Home

Krafton acquires minority stake in Forever Skies developer Far From Home

Apr 22, 2024

|

2 Min Read

by

Chris Kerr

Sponsored Content

Live service developers are increasingly looking to buy rather than build

Live service developers are increasingly looking to buy rather than build

Apr 22, 2024

|

7 Min Read

Business

Kabam is taking Marvel: Contest of Champions to 'alternative' app stores

Kabam is taking Marvel: Contest of Champions to 'alternative' app stores

Apr 19, 2024

|

1 Min Read

by

Justin Carter

Design

Overwatch 2 players who use 'unapproved peripherals' could receive permanent bans

Overwatch 2 players who use 'unapproved peripherals' could receive permanent bans

Apr 19, 2024

|

3 Min Read

by

Chris Kerr

Business

Devolver financials show stable 2023, despite 'quiet' first-half

Devolver financials show stable 2023, despite "quiet" first-half

Apr 18, 2024

|

2 Min Read

by

Justin Carter

Business

Modern Wolf lays off six staff in studio restructuring

Modern Wolf lays off six staff in studio restructuring

Apr 18, 2024

|

1 Min Read

by

Justin Carter

Business

Playdate devs have earned over $500,000 through Catalog

Playdate devs have earned over $500,000 through Catalog

Apr 18, 2024

|

2 Min Read

by

Chris Kerr

Business

UK Games Fund grants £3 million to 22 'rising' game developers

UK Games Fund grants £3 million to 22 'rising' game developers

Apr 17, 2024

|

1 Min Read

by

Justin Carter

Business

Sea of Thieves sails to 40 million players ahead of PS5 launch

Sea of Thieves sails to 40 million players ahead of PS5 launch

Apr 17, 2024

|

1 Min Read

by

Justin Carter

Business

Ghost of Tsushima's PC port introduces new PlayStation overlay, trophy support

Ghost of Tsushima's PC port introduces new PlayStation overlay, trophy support

Apr 17, 2024

|

1 Min Read

by

Justin Carter

Business

Ready or Not source code stolen in developer hack

Ready or Not source code stolen in developer hack

Apr 17, 2024

|

1 Min Read

by

Justin Carter

Design

Warren Spector says the next logical step for immersive sims is multiplayer

Warren Spector says the next logical step for immersive sims is multiplayer

Apr 16, 2024

|

6 Min Read

by

Bryant Francis

Business

Rovio's Moomin mobile game goes offline in July

Rovio's Moomin mobile game goes offline in July

Apr 16, 2024

|

1 Min Read

by

Justin Carter

Business

70 percent of devs unsure of live-service games sustainability

70 percent of devs unsure of live-service games sustainability

Apr 16, 2024

|

2 Min Read

by

Justin Carter

Business

Descent 3's source code has been released for free use

Descent 3's source code has been released for free use

Apr 16, 2024

|

2 Min Read

by

Justin Carter

Business

Roblox introducing new 'publishing advance' fee as it opens up creator marketplace

Roblox introducing new 'publishing advance' fee as it opens up creator marketplace

Apr 16, 2024

|

3 Min Read

by

Chris Kerr

Business

Fallout games double in player count after Prime series premiere

Fallout games double in player count after Prime series premiere

Apr 15, 2024

|

2 Min Read

by

Justin Carter

Business

Rockstar quietly bumps up GTA Online's subscripion price

Rockstar quietly bumps up GTA Online's subscripion price

Apr 15, 2024

|

1 Min Read

by

Justin Carter

Business

Skybound turns to crowdfunding for triple-A Invincible game

Skybound turns to crowdfunding for triple-A Invincible game

Apr 15, 2024

|

2 Min Read

by

Justin Carter

Previous

1

2

3

4

5

…

1050

Next

Latest News

A city fighting back the cold in Frostpunk

Business

Frostpunk has topped 5 million sales in six years

Frostpunk has topped 5 million sales in six years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Key artwork for Garry's Mod

Business

Nintendo's legal team is coming for Garry's Mod after 20 years

Nintendo's legal team is coming for Garry's Mod after 20 years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Get daily news, dev blogs, and stories from Game Developer straight to your inbox

Subscribe to Game Developer Newsletters to stay caught up with the latest news, design insights, marketing tips, and more

Stay Updated

Trending

A city fighting back the cold in Frostpunk

Business

Frostpunk has topped 5 million sales in six years

Frostpunk has topped 5 million sales in six years

by

Chris Kerr

Apr 25, 2024

2 Min Read

Key artwork for Garry's Mod

Business

Nintendo's legal team is coming for Garry's Mod after 20 years

Nintendo's legal team is coming for Garry's Mod after 20 years

by

Chris Kerr

Apr 25, 2024

2 Min Read

A Steam Deck in action

Business

Valve updates Steam refund policy to cover 'Advanced Access' playtime

Valve updates Steam refund policy to cover 'Advanced Access' playtime

by

Chris Kerr

Apr 24, 2024

2 Min Read

Featured Blogs

Design

Murder on Space Station 52 - Paper to Pixel: Making a Scene

Murder on Space Station 52 - Paper to Pixel: Making a Scene

Apr 24, 2024

player using a handheld device

Business

How handheld gaming has become more complex – and more lucrative

How handheld gaming has become more complex – and more lucrative

Apr 24, 2024

Design

The Six Stages of Player Rationality

The Six Stages of Player Rationality

Apr 19, 2024

Daily news, dev blogs, and stories from Game Developer straight to your inbox

Stay Updated